Emergency fund essentials

Why you need this financial buffer.

Imagine this scenario: the muffler falls off your car on the way to work, you get home at the end of a busy day only to discover that the fridge has broken down, the dog is sick and needs to visit the vet, and your employer is signalling that there might be some downsizing at work. Suddenly you’re facing a mountain of unexpected bills and concerns about employment stability – without a safety net.

Maybe you’ve always meant to set aside a bit of money for a rainy day or some kind of emergency, but just haven’t gotten around to it. Take heart knowing that you’re not alone in setting this task on the back burner. Perhaps unsurprisingly, a recent survey found that nearly half of Canadians said they would struggle to handle unexpected expenses.[1]

The good news is that it’s never too late to start building an emergency fund. The first step is determining your needs.

What’s a good amount?

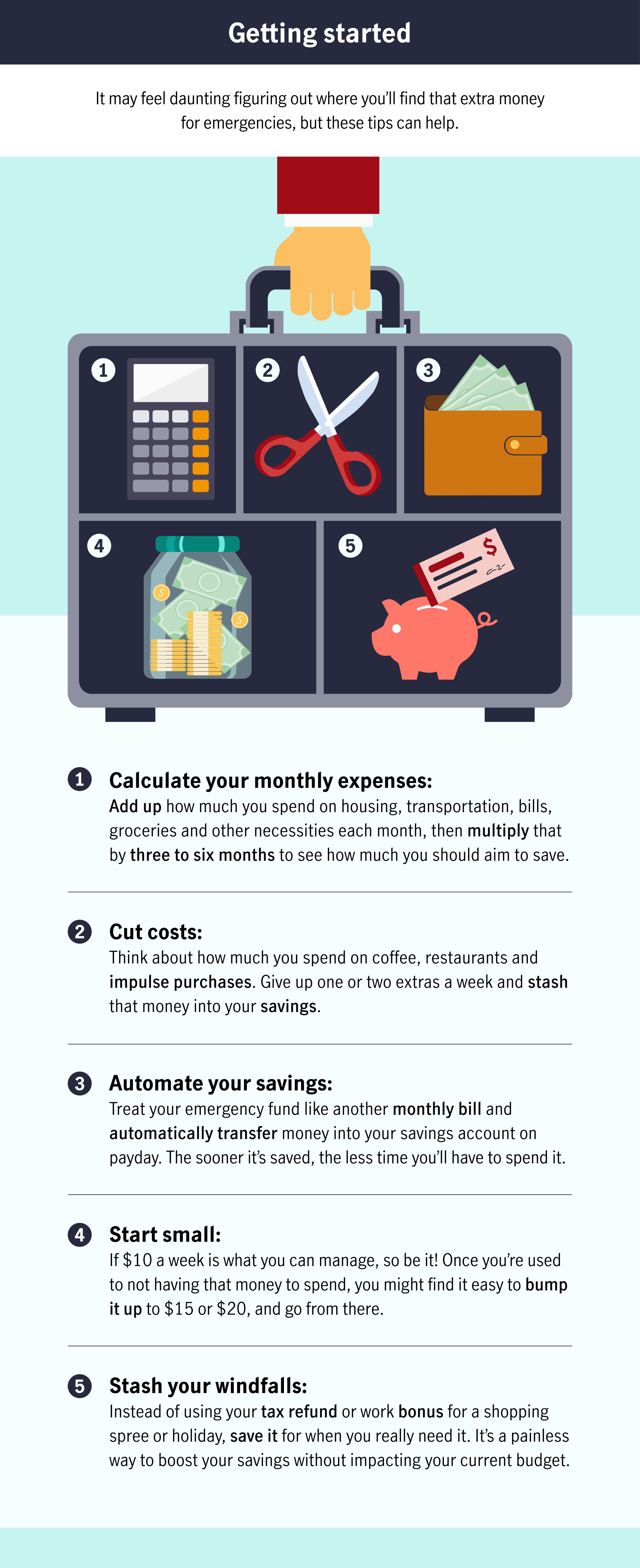

The gold standard for an emergency fund covers between three to six months of expenses. This amount might seem large, but it provides a solid buffer in case you or your spouse lose a job, face an injury or illness, or encounter a lot of unplanned expenses all at once.

Consider your household budget and what you can realistically afford to set aside for emergencies. Even a small amount, such as $10 a week, is a good place to start, and you can add to it over time. As you determine what you can afford to pay into an emergency fund, don’t overlook other financial goals you’ve put in place such as regular investment contributions and debt repayment.

Consider the power of automated weekly contributions. Depositing $20 a week automatically into your emergency fund amounts to $960 annually.*

* This doesn’t include the interest you may earn.

Where to keep an emergency fund

Most people have chequing and savings accounts as part of their normal banking routine. For an emergency fund, you’ll want to establish an account that’s available if you really need it, but clearly separate from the funds used for household expenses and short-terms goals such as vacations or home improvements. Consider these options:

High interest savings account : Contact your advisor about setting up an account that’s separate from your day-to-day transactions. Remember to ask about the account interest rate and whether there are any transaction fees or penalties for withdrawals.

TFSA (Tax-Free Savings Account): This flexible savings account allows you to withdraw funds at any time – and any investment growth that accumulates can be withdrawn tax-free. Currently, the annual TFSA contribution amount is $6,000. However, if you’ve never contributed before, you could have as much as $81,500 in contribution room dating back to 2009, when the TFSA was first introduced. Be cautious of contributing more than the amount available to you to avoid financial penalty. Investments that can be held within a TFSA include high interest savings accounts, stocks, bonds, mutual funds and guaranteed investment certificates. Talk to your advisor about what makes sense for financial stability while continuing to grow funds within the account.

Review your goals

Make it a habit to review your household budget periodically to ensure you’re still making emergency fund savings a priority as changes occur in your life. Raising children, buying a home, adopting pets, general inflation and other factors may increasingly impact your ability to save.

Think about where you can find savings in other ways – check out this article to learn a few supersaver secrets. Finding a bit of extra money for the emergency fund could also be as simple as dropping any loose change into a container at the end of the day or gathering up and selling items around the house that you no longer need. One person’s clutter is another person’s treasure, and your emergency fund will get a nice boost in the process.

Saving up for the unexpected can be easier than you think, and if or when a crisis happens, you’ll be very glad you did. As always, your advisor is there to help you plan your financial future and decide how everything, including your emergency fund, fits into your household budget.

[1] www.manulifebank.ca/personal-banking/plan-and-learn/personal-finance/spring-debt-survey.html